Spending Review 2020: Managing uncertainty

COVID-19 and the NHS long term plan

24 November 2020

About 27 mins to read

Key points

- The coronavirus (COVID-19) pandemic has already led to significant costs for the NHS in 2020/21, with increased spending of at least £34.9bn – almost 24% of the planned health budget this year. For this financial year as a whole COVID-19 costs for the health system could be in the region of around £47bn.

- The biggest areas of spending have been NHS Test and Trace (£12bn) and PPE (£15bn). Even with a vaccine on the horizon, there will be ongoing COVID-19 costs for the health system in 2021/22. Maintaining a test and trace system, ensuring infection prevention and control measures are sustained, delivering sufficient capacity and rolling out any prospective vaccine will all require further funding. The total direct costs associated with managing the pandemic could be around £27bn next year.

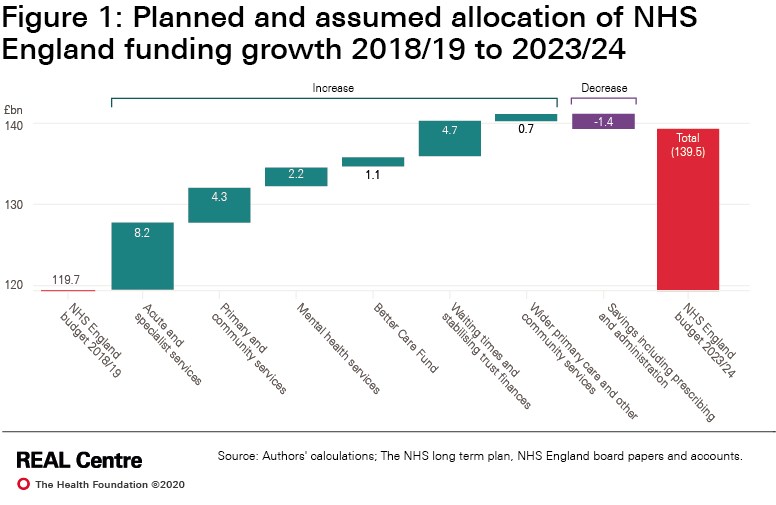

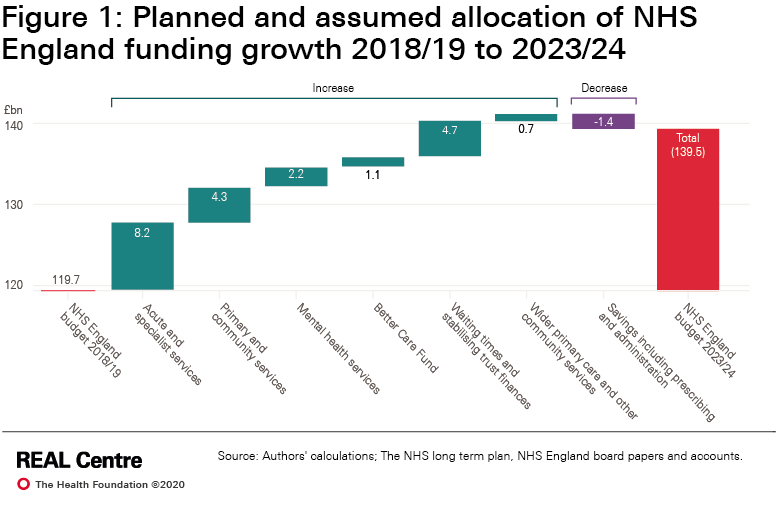

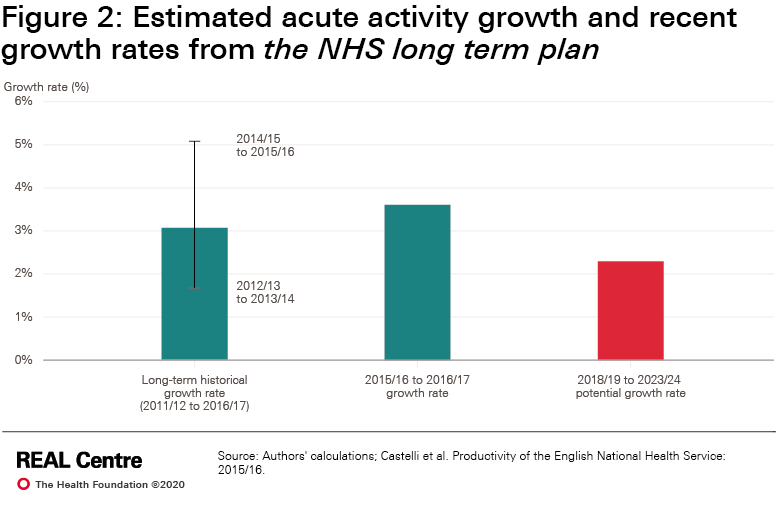

- While vital, this spending does not contribute to the NHS long term plan aims of transforming and modernising services, while meeting underlying demand. At the start of the pandemic the NHS was entering the second year of the plan, backed by real-terms funding growth of 3.3% per year for NHS England’s budget. The pandemic has made delivering the long term plan much more challenging and will require significant extra funding.

- The number of patients the NHS can treat has inevitably fallen as COVID-19 has placed new demands on the health system and changed the way care is provided. NHS productivity is likely to be lower in 2021/22 and 2022/23. If productivity falls by 5% in 2021/22 this would increase funding needs by around £7bn. Catching up lost productivity will take time and by 2023/24 front-line NHS services will need £3bn more than currently allocated to deliver core services.

- The pandemic has led to a backlog of care. For elective care there are 4.7 million ‘missing patients’ who have not been referred for treatment (compared with 2019). If three-quarters of these patients are referred for treatment in the coming months, the waiting list could grow to 9.7 million by 2023/24.

- Waiting times are also increasing with 45% of patients now waiting more than 18 weeks. Meeting the 18-week standard by 2023/24 is not achievable – even if the Treasury was prepared to provide all the funding required. It would require an annual average 11% increase in the number of elective procedures being performed each year by the NHS, needing some 4,000 extra consultants and 17,000 extra nurses a year. We estimate that it is more realistic to achieve the waiting time standard and eliminate the backlog of long waits over a 6-year period, ending in 2026/27. To achieve this NHS England would require an additional £900m on top of the current spending plans.

- The mental health consequences of the pandemic are a source of considerable concern. On average over the next 3 years we estimate that there could be 11% more referrals a year, costing between £1.1 and 1.4bn extra each year.

- Excluding the costs associated with directly managing COVID-19, restoring waiting times, additional mental health demand and lower productivity will cost around £10bn extra next year, if the NHS is to have sufficient resources to deliver the long term plan.

- The extra money for front-line NHS services needs to be matched with up to £1bn extra a year in each of the next 3 years for the workforce, up to £3bn extra for public health and an additional £1bn a year for capital investment in the NHS. Without investment in these areas, the NHS will not deliver the ambitions in the long term plan and will lack resilience for future health shocks.

- We estimate the overall additional cost pressures for the health budget as a whole in the wake of COVID-19 in the overview chart below.

- This year and next COVID-19 is likely to result in extra health costs of around £40bn a year –around 2% of pre-COVID-19 GDP. Most of these costs are temporary but not all. COVID-19 is likely to lead to an increase in NHS funding pressures over the medium term of around 0.5% of GDP.

- There are choices and trade-offs about both the short and long term. If the government wants services to recover quickly and run as fully as possible this winter and next year, the NHS will need more funding. Beyond the pandemic the scale of additional costs depends on the government’s decisions about waiting times and its long term plan commitment to modernise and transform services.

All numbers in this long read are in 2020/21 prices using the October 2020 GDP deflators at market prices. It was published on 24 November 2020.

Overview: overall additional cost pressures for the health budget

Further reading

Spending Review 2020: Managing uncertainty

Work with us

We look for talented and passionate individuals as everyone at the Health Foundation has an important role to play.

View current vacanciesThe Q community

Q is an initiative connecting people with improvement expertise across the UK.

Find out more

{kind=link}

{kind=link}