What should be done to fix the crisis in social care?

Five priorities for government

What should be done to fix the crisis in social care?

30 August 2019

About 15 mins to read

Key points

- Adult social care in England needs fixing – and has done for decades. Increasing numbers of people are unable to access social care and care providers are at risk of collapse. Yet successive governments continue to duck reform, and people and their families continue to suffer unnecessarily.

- Based on our assessment of the evidence and analysis of the costs of reform, five priorities for government are:

- stabilising and sustaining the current system

- improving access to care

- providing social protection against care costs

- seeing the capped cost model as a flexible approach to reform

- exploring a range of options for raising revenue.

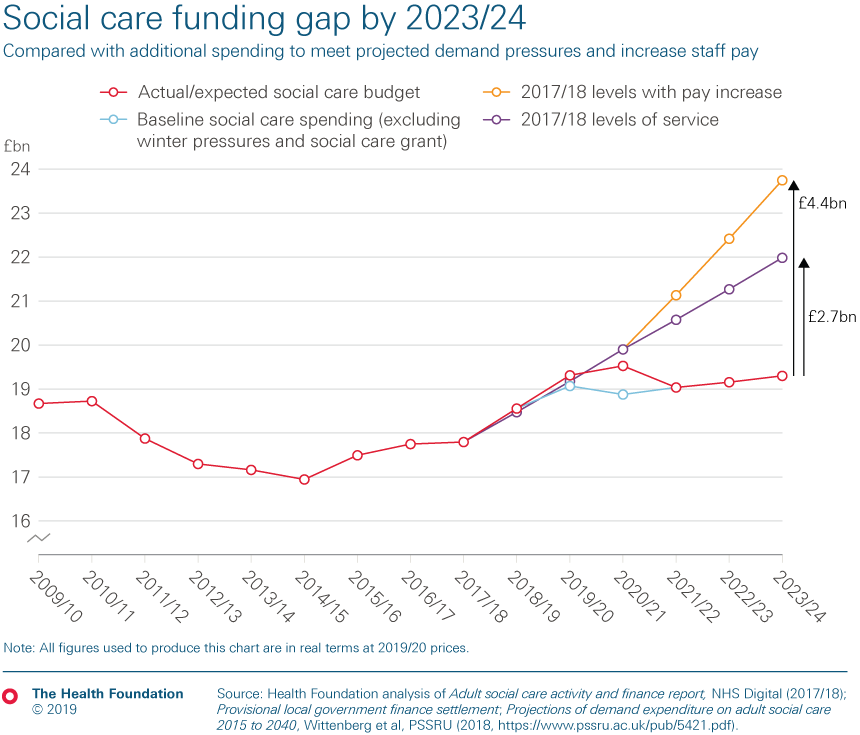

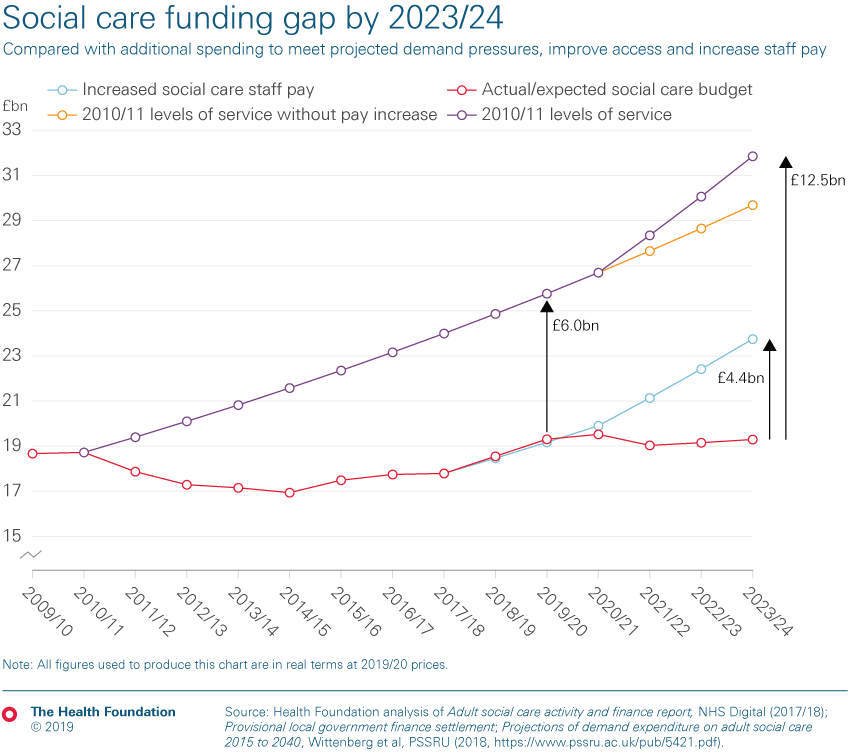

- The immediate priority for government should be to stabilise and improve the current system, including by boosting staff pay and improving access to publicly funded care. Stabilising the current system by addressing demand pressures and increasing staff pay in line with the NHS would cost £1.0bn in 2020/21, £2.1bn in 2021/22 rising to £4.4bn in 2023/24, compared to the current baseline budget. Restoring access to 2010/11 levels of service would require around £8.1bn extra investment by 2023/24 on top of this (£12.5bn in total). (See our latest analysis on the 2019 Spending Round).

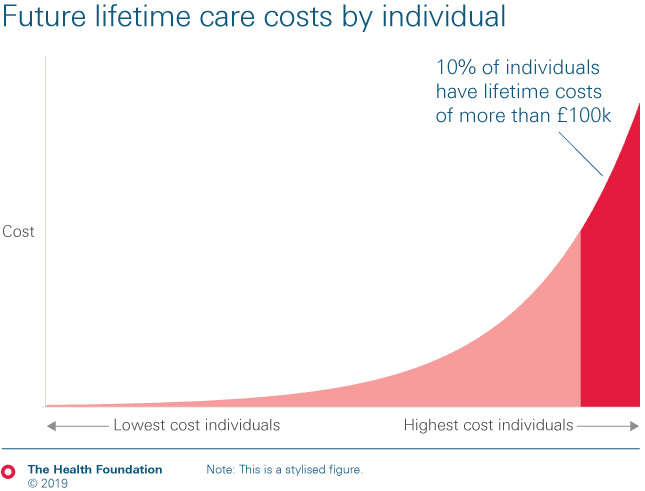

- But more fundamental reform is needed to make the funding system fairer and provide government protection against social care costs. Policymakers have choices on how to do this, based on their values, priorities, and public spending plans. A Dilnot-style capped cost model – which focuses extra state funding on those with the greatest lifetime care needs and protects them from bearing costs above a certain limit – could be used flexibly by any government, and already lies on the statute book.

- Any credible reform option requires government investment. The cost of implementing a Scottish-style model, for example, could add around £4.4bn to spending in 2019/20, rising to £5bn by 2023/24. The cost of a Dilnot-style model depends on where you set the cap to protect people against steep costs of care – ranging from around £1.7bn in 2019/20 rising to £2.1bn by 2023/24 under the least generous scenario (a £78,000 cap), to £6.8bn in 2019/20 rising to £7.8bn in 2023/24 under the most generous (a £0 cap – where the state covers all costs of a person's eligible needs).

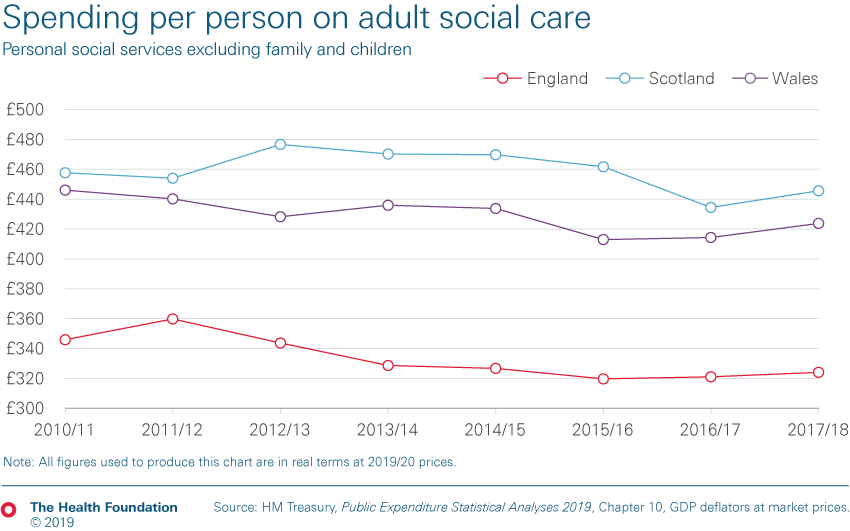

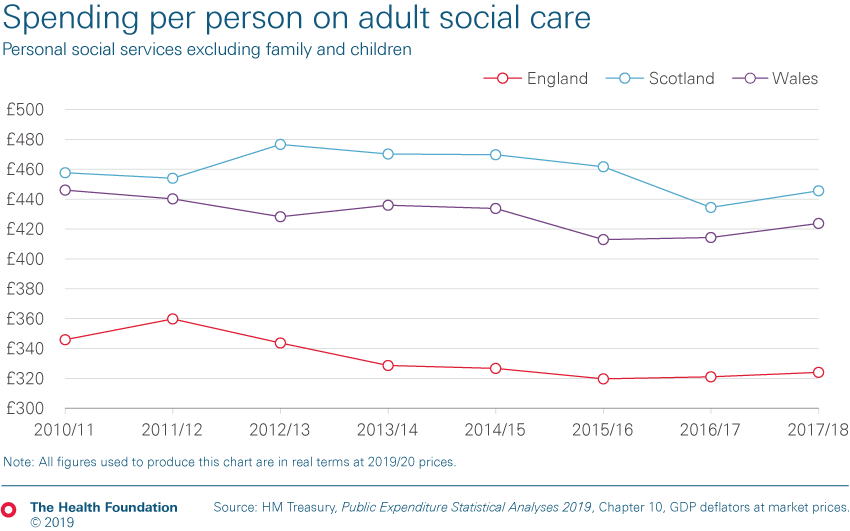

- Public spending on services in England was £525bn in 2017/18 (in today's prices). Of that, we spent around £18bn on adult social care. Across the whole UK, we spent £22.7bn on social care – 1.1% of GDP. This compared to wider health spending in 2017/18 of £153bn, equivalent to 7.1% of GDP – and projected to grow to 7.9% in 2023/24.

- A range of options can be explored to raise revenue to fund social care reform. Increases in taxation would be an obvious route to paying for a more generous and fairer system.

- Reform is often thought to be unaffordable. But if it chooses, the government can afford to provide more generous care, support and security for vulnerable people in society. If it doesn't, it will be choosing to prolong one of the biggest public policy and political failures of our generation.

What should be done to fix the crisis in social care?

1. Introduction

2. 1. Stabilise and sustain the current system

3. 2. Improve access to care

4. 3. Provide social protection against care costs

5. 4. See the capped cost model as a flexible approach to reform

6. 5. Explore a range of options for raising revenue

7. Where next?

8. Downloads and related content

Work with us

We look for talented and passionate individuals as everyone at the Health Foundation has an important role to play.

View current vacanciesThe Q community

Q is an initiative connecting people with improvement expertise across the UK.

Find out more

{kind=link}

{kind=link}

{kind=link}

{kind=link}